January 2, 2026

Roof Repair vs Replacement: Why the Wrong Choice Costs You More Than Money

Author

A leak shows up on your ceiling, and suddenly you’re facing the classic homeowner dilemma: roof repair or full replacement. One option might cost a few hundred or a couple thousand dollars. The other could run well into five figures.

On the surface, the decision feels simple—fix the problem and move on. But roofing decisions rarely stay that simple for long.

What many homeowners don’t realize is that choosing repair or replacement affects far more than the immediate leak. The choice influences your home’s resale value, insurance claims, energy efficiency, and how much you’ll spend on roofing over the next 10–20 years. In many cases, the “cheaper” option today quietly creates bigger costs later.

The key is understanding what your roof is actually telling you—whether the problem is isolated damage that a repair can solve or a larger system failure that patching won’t fix. Knowing the difference can save you thousands and prevent the cycle of repeated repairs that homeowners often fall into.

If you're already dealing with an active leak, it’s important to address it quickly before evaluating long-term solutions. Our guide on emergency roof leak repair and how to stop a leak in the rain explains what you can do right away to minimize damage.

Table of Contents

- TL;DR

- The Hidden Cost No One Warns You About

- Reading the Signals Your Roof Is Already Sending

- The Repair Trap (And When Patching Actually Makes Sense)

- Replacement Isn't Always the Nuclear Option

- What Your Insurance Company Isn't Telling You

- The Timeline Factor Most Homeowners Ignore

- How We Help You Make the Right Call Without the Sales Pressure

TL;DR

- Roof decisions impact your home's resale value, energy efficiency, and structural integrity for 15+ years, not just your immediate problem

- Multiple repairs in a short timeframe often signal systemic failure that patching can't fix

- Insurance claims favor replacement over repair in specific damage scenarios, but timing your claim matters

- Partial replacements exist as a middle ground but only work under certain conditions

- The age of your roof relative to its expected lifespan should drive 60% of your decision

- Delaying a needed replacement to "get one more year" typically doubles your eventual cost

The Hidden Cost No One Warns You About

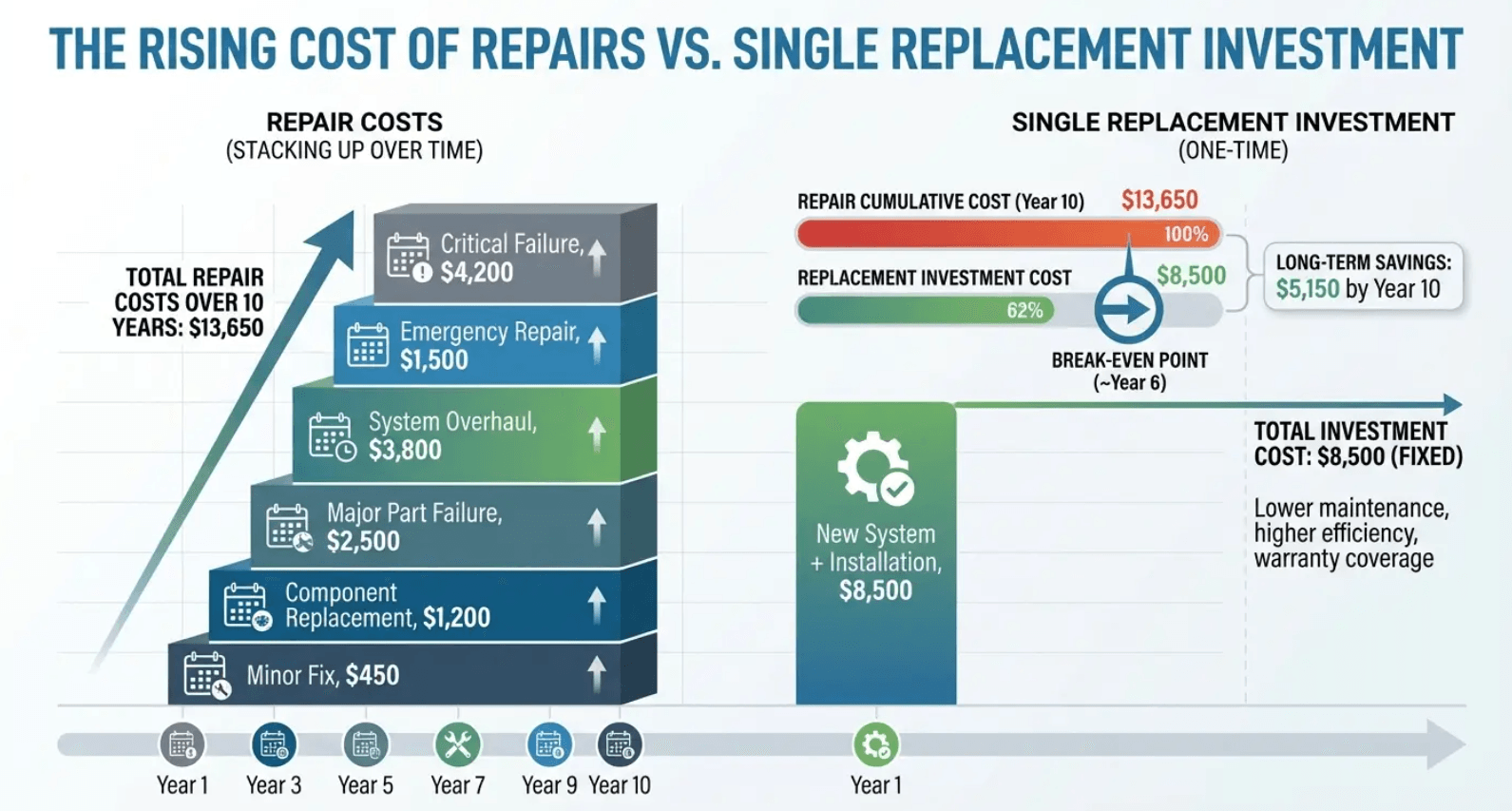

$1,200 or $12,000.

That's what the roofer just told you, and the choice seems obvious, right? Fix it for twelve hundred bucks, get another few years, worry about replacement later.

Except that's not actually what you're choosing between.

Every roofing decision you make today locks you into a trajectory that affects your home's value, your insurance rates, and your options when you eventually sell. I've seen homeowners spend three grand on repairs over two years, then face a full replacement anyway... but now they're doing it during a market spike or right before listing their house.

The real cost isn't the check you write today. It's the flexibility you lose tomorrow.

Most homeowners fixate on the upfront price difference without considering how their choice affects future flexibility, home value, insurance premiums, and the compounding effect of putting off decisions.

Why Your Future Self Might Regret the "Cheaper" Option

Repairs buy you time, but they don't reset anything. Your 18-year-old roof with a fresh patch is still an 18-year-old roof. Prospective buyers see that age during inspection, and they either negotiate down or walk away.

Insurance companies track your claim history. File three repair claims in five years, and you're flagged as high-risk. That affects your premiums even after you finally replace the roof. I've watched homeowners save eight thousand on a repair decision, then lose twelve thousand in negotiating power when they sold three years later.

I worked with a family in Portland last year (won't use names, but they know who they are) who spent $1,800 fixing storm damage to their 16-year-old roof. Six months later, different leak, different section, another $1,400. When they listed their home, the inspector flagged the aging roof, and buyers knocked $9,000 off the asking price. They spent $3,200 on repairs and lost $9,000 in sale value. That's a $12,200 mistake on a roof replacement that would've cost $11,000.

Energy efficiency takes a hit too. Older roofing materials with spot repairs create hot spots and cold spots. Your HVAC system works harder. You're bleeding money every month, but it's invisible compared to a one-time roofing invoice.

Patchwork repairs create irregular wear patterns that make future work more expensive. They complicate insurance claims down the line. They affect buyer perception during home sales in ways that cost you thousands at the negotiating table.

The Replacement Benefit Nobody Talks About

Replacement does something repair never can: it gives you a complete do-over. You're not just fixing the visible problem. You're addressing the rot in the decking you didn't know existed, upgrading ventilation that's been inadequate since the house was built, and installing materials that meet current code (which matters more than you think).

You get a transferable warranty. That's a selling point buyers actually care about, especially if you're planning to move within ten years. New roofs also qualify for better insurance rates in many markets, particularly in storm-prone areas where impact-resistant materials earn you discounts.

| Repair Approach | Replacement Approach |

|---|---|

| Addresses visible symptoms only | Fixes underlying structural issues |

| No warranty reset on existing materials | Full warranty on all new materials (typically 15-30 years) |

| Cannot upgrade ventilation or code compliance | Opportunity to meet current building codes |

| Maintains existing energy efficiency gaps | Improves thermal performance and energy costs |

| No impact on insurance rates | May qualify for premium discounts (5-20% in some markets) |

| Leaves hidden damage undetected | Allows full decking and structure inspection |

There's also the mental calculus. Replacing your roof removes it from your list of "things that might fail catastrophically." You're not watching weather forecasts with dread or wondering if this is the year everything falls apart. That peace of mind has value, even if it doesn't show up on a spreadsheet.

Modern materials improve thermal performance in ways that older roofs simply can't match. I'm seeing homeowners reduce cooling costs by 10, maybe 15 percent after replacement with properly ventilated, reflective materials. That savings compounds year after year.

Reading the Signals Your Roof Is Already Sending

Your roof's talking to you. Most people just don't speak roof.

The difference between isolated damage and systemic failure determines whether you're looking at a two-thousand-dollar fix or a fifteen-thousand-dollar replacement, and misreading those signals costs you.

Isolated Damage vs. Systemic Failure

A single missing shingle from last month's windstorm? That's isolated. You can repair that without losing sleep.

Curling shingles across your entire south-facing slope? That's your roof telling you it's cooked. Literally. UV exposure has broken down the asphalt, and patching won't stop the spread.

So your gutters are full of what looks like sand. That's... not great.

A little bit of granule loss is normal. Shingles shed when they're new. But if you're scooping out coarse sand every few months, your shingles are disintegrating. That's systemic, and it's accelerating.

Here's what you're looking for:

□ Gutters: Check for granule accumulation. Small amounts are normal, but if you could build a sandcastle with what's in there, your roof is falling apart.

□ Shingles: Stand back and look at the whole roof. Are shingles curling in multiple spots, or just where that tree branch hit? Scattered damage means aging. Localized damage means repairable event.

□ Pattern recognition: Does the damage match recent weather events, or does it look age-related? If your neighbors' roofs of similar age look the same, that's normal aging.

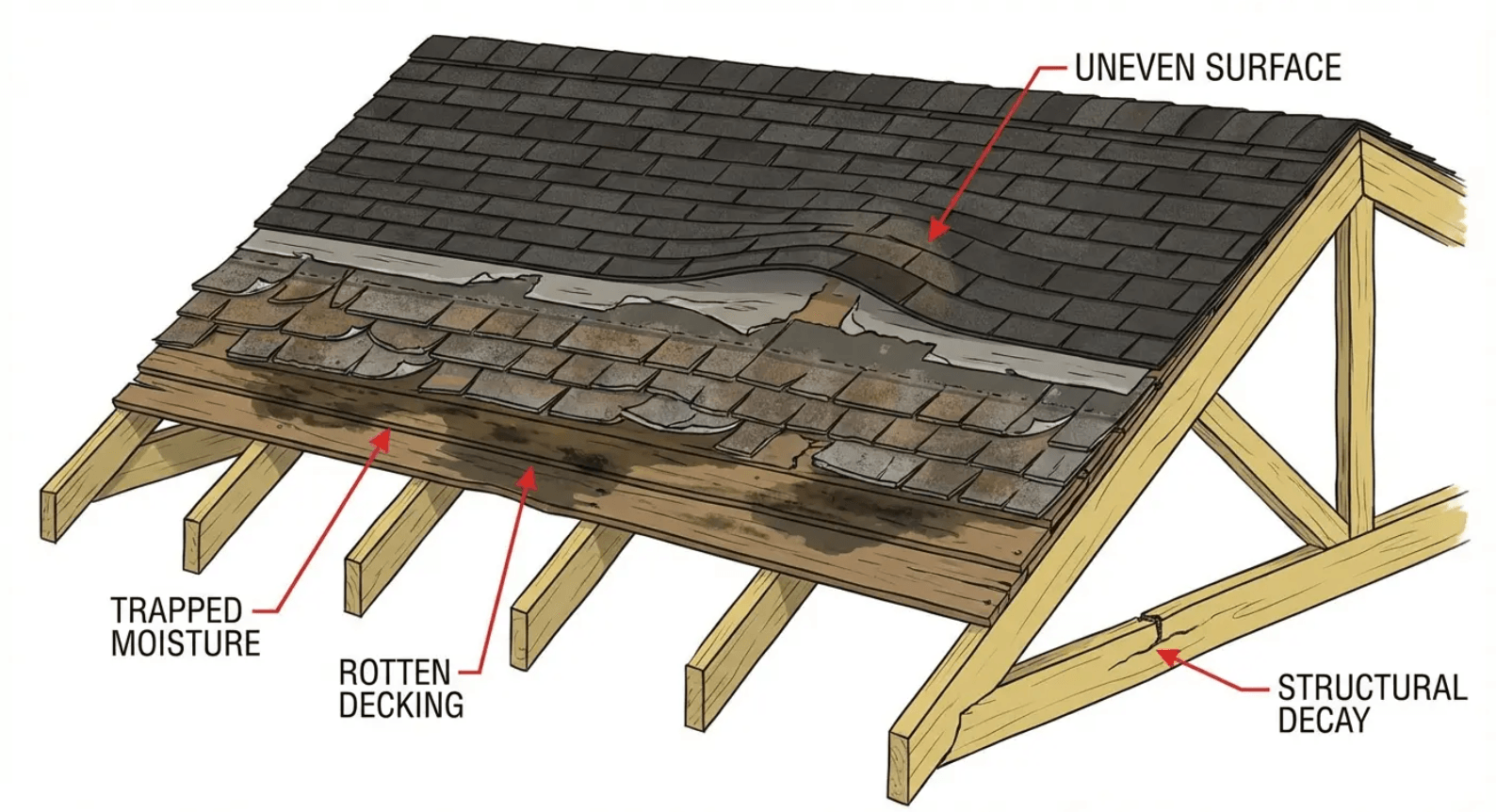

□ Attic inspection: Go up there with a flashlight. See daylight coming through anywhere? Water stains on multiple sections of decking? That's bad.

□ Structural concerns: Any sagging, dipping, or uneven areas in the roofline need immediate attention.

Damage concentrated around one area (where a tree branch hit, for example) suggests a repair scenario. Damage scattered across multiple roof planes, especially if it's the same type of wear, means your roof is aging out uniformly. You can't repair your way out of old age.

The location of damage matters more than most people realize. Damage on north-facing slopes often indicates different problems than south-facing damage. North slopes hold moisture longer, leading to algae growth and shingle degradation from biological sources. South slopes cook under direct sun, causing thermal breakdown of the asphalt.

The Age Question Everyone Gets Wrong

Your 25-year shingles aren't guaranteed to hit 25 years. That's a best-case scenario assuming perfect installation, ideal climate, and proper maintenance. In reality, you're looking at 18-22 years in most conditions. Less if you're in an extreme climate zone.

Different roofing materials have vastly different lifespans that affect replacement timing decisions

This is how I think about it: If your roof is past 75% of its expected lifespan and you're facing a repair that costs more than 15% of replacement cost, replacement makes more sense. The math changes if you're at 50% lifespan, but even then, you need to consider how many years the repair actually buys you.

Climate, installation quality, ventilation, and maintenance affect longevity in ways that manufacturer ratings don't capture. I've seen "30-year" roofs fail at year 14 in harsh sun exposure. I've also seen well-maintained roofs in ideal conditions exceed their rated lifespan by five years.

A homeowner in Denver had a 17-year-old asphalt shingle roof (rated for 25 years, so 68% through expected lifespan) with localized hail damage estimated at $2,800 to repair. Full replacement was quoted at $14,500. The repair represented 19% of replacement cost, and the roof was approaching the 75% lifespan threshold. Two years later, they faced another $3,100 in repairs for wind damage to a different section. By waiting, they spent $5,900 on repairs for a roof that still needed replacement at year 19, when they could have replaced it once at year 17 and been done.

Don't wait for total failure.

I'm serious. Waiting until your roof completely dies means you're dealing with emergency pricing, water damage to your interior, and calling contractors who know you're desperate. You have zero leverage. I've seen homeowners spend literally double what they would've spent if they'd replaced it six months earlier when they first started noticing problems. It's brutal to watch.

Understanding the repair vs replacement decision hinges on evaluating whether a roof at 60%, 75%, or 90% of its expected life is a repair or replacement candidate, factoring in the extent of current damage. A roof at 90% of expected lifespan with even minor damage is a replacement candidate. A roof at 60% with isolated storm damage is a repair candidate. The gray area between 70-85% requires honest assessment of damage extent and your timeline for the home.

The Repair Trap (And When Patching Actually Makes Sense)

I'm about to tell you when repairs actually make sense, which is weird because I'm a roofer and I make more money on replacements.

But here's the thing: I'm tired of homeowners getting sold replacements they don't need. It makes the whole industry look predatory, and it pisses me off.

That's the industry perspective. From where I stand, working with homeowners daily, the question isn't whether roofs can be repaired. It's whether they should be.

The Only Three Scenarios Where Repair Wins

Storm damage on a seven-year-old roof? Repair it. No question. You've got potentially 15+ years of life left, and insurance is probably covering most of the cost anyway. The damage is event-based, not age-based, so fixing it doesn't just kick the can down the road.

Warranty-covered installation defects are obvious repair candidates, but only if your warranty is enforceable and the contractor is still in business. I've seen too many homeowners discover their "lifetime warranty" died when the company dissolved. (Pro tip: check that before you assume you're covered.)

Selling soon creates different math. If you're listing in six months, a $2,000 repair that gets you through inspection makes more sense than a $15,000 replacement you won't recoup. But be honest about your timeline. "Might sell in the next few years" doesn't count. You need a signed listing agreement or you're fooling yourself.

| Scenario | Roof Age | Damage Type | Repair Cost Threshold | Decision |

|---|---|---|---|---|

| Storm damage (isolated) | Under 10 years | Event-based (wind, hail, tree impact) | Less than 20% of replacement cost | Repair |

| Warranty defect | Any age | Installation error, material defect | Covered by valid warranty | Repair |

| Pre-sale preparation | Any age | Cosmetic or minor functional issues | Less than $3,000 with sale within 6-12 months | Repair |

| Multiple problem areas | Over 15 years | Age-related wear across roof planes | Exceeds 30% of replacement cost | Replace |

| Recurring leaks | Over 12 years | Same or different areas, multiple repairs in 3 years | Cumulative repairs exceed 25% of replacement | Replace |

These three scenarios share a common thread: the underlying roof system is fundamentally sound, and the damage or issue is genuinely isolated. Outside these scenarios, you're probably looking at replacement territory.

How to Know You're Already in the Trap

Add up what you've spent on roof repairs in the past three years. If that number exceeds 30% of what replacement would cost, you're in the trap. You're paying replacement prices on an installment plan, but you're not getting a new roof out of it.

How often are you calling roofers? If it's moved from "once every few years" to "twice a year," your roof is failing progressively. Each repair is a temporary plug in a deteriorating system.

Figure out if you're in the repair trap:

1. Calculate Your 3-Year Repair Total:

- Repair #1: $_______ (Date: ______)

- Repair #2: $_______ (Date: ______)

- Repair #3: $_______ (Date: ______)

- Total Spent: $_______

2. Get Replacement Cost Estimate: $_______

3. Calculate Repair-to-Replacement Ratio:

- (Total Repairs ÷ Replacement Cost) × 100 = _______%

- If over 30%: You're in the repair trap

4. Assess Repair Frequency:

- Number of repair calls in past 3 years: _______

- If 3 or more: Progressive failure pattern

5. Identify Repair Pattern:

- □ Same location repaired multiple times (symptom treatment)

- □ Different locations each time (systemic failure)

- Either pattern after year 15 = replacement candidate

6. Factor in Roof Age:

- Current roof age: _______ years

- Expected lifespan: _______ years

- Percentage of lifespan used: _______%

- If over 75% + repairs needed: replace now

Are you fixing new problems, or are you re-fixing the same areas? If water keeps finding its way into the same bedroom despite two previous repairs, you're treating symptoms while the disease spreads. That's not a repair situation anymore. That's your roof telling you it's done.

The financial impact of repair cycles can be substantial.

I've had homeowners show me receipts spanning five years, totaling nine grand in repairs, all while avoiding the thirteen-thousand-dollar replacement conversation. They thought they were being financially prudent. They were hemorrhaging money while their roof continued deteriorating.

Replacement Isn't Always the Nuclear Option

The assumption that replacement means tearing off and replacing the entire roof stops a lot of homeowners from considering it. There are middle-ground options that work under specific conditions. Key word: specific.

Partial Replacement: The Middle Ground That Actually Works

Partial replacement works when damage or aging is legitimately confined to one section of your roof. I'm talking about replacing an entire plane or section, not just patching a few squares. This makes sense when you've got a complex roof where one section gets dramatically different sun exposure or weather impact than others.

The challenge? Material matching. Shingle manufacturers change product lines, and even if you find the same model, the color might not match after a few years of weathering. You'll have visible lines where old meets new. Some homeowners don't care. Others hate it.

Cost-wise, you're typically looking at somewhere between 40-60% of full replacement cost for partial work. That's not the bargain it might seem. You're paying mobilization costs, and you're not resetting the clock on the sections you didn't replace. Run the numbers carefully. If partial replacement costs 55% of full replacement but only extends your roof life by 30%, the math doesn't work.

A homeowner in Phoenix with a multi-level home had severe UV degradation on the west-facing slope of their roof after 14 years, while the east and north slopes showed minimal wear. They opted for partial replacement of just the west plane at $6,800 (compared to $15,200 for full replacement, about 45% of total cost). Five years later, the other slopes began failing, and they paid $12,400 for full replacement (prices had increased). Total spent: $19,200 over five years. Had they replaced the entire roof initially, they would have saved $4,000 and had a uniform warranty across all planes.

Partial replacement only makes financial sense when the undamaged sections have at least 10 years of viable life remaining and the damaged section represents a distinct architectural feature with different exposure conditions. Otherwise, you're just delaying the inevitable while paying premium per-square-foot pricing.

Why Overlays Aren't the Shortcut You Think They Are

Overlay means installing new shingles directly over your existing layer. It's cheaper upfront because you skip tear-off and disposal costs. It's also a gamble you'll probably lose.

You can't inspect the decking underneath. Any rot, water damage, or structural issues stay hidden until they become catastrophic. The new shingles don't last as long either because they're sitting on an uneven surface that traps heat. You might get 15 years from shingles rated for 25.

When you eventually replace (and you will), you're paying to remove two layers instead of one. That increased disposal cost often erases the savings you thought you were getting. Some jurisdictions don't allow it at all. If you've already got two layers, overlay isn't even an option.

I've seen overlay work in exactly one scenario: when a homeowner needed to pass inspection for an immediate sale and the existing roof had no structural issues but looked cosmetically poor. They spent $7,000 on overlay, sold within 60 days, and disclosed the overlay to buyers. That's strategic. Everything else is wishful thinking.

What Your Insurance Company Isn't Telling You

Look, I'm gonna be straight with you about insurance companies.

Insurance dynamics affect the repair vs replacement decision in ways most homeowners don't understand until they're already filing a claim. The timing of your claim, the age of your roof, and the specific language in your policy all matter more than the extent of damage in some cases.

How Roof Age Affects Your Claim Payout

Insurance companies depreciate roofs annually. A 15-year-old roof on a 25-year shingle typically gets valued at maybe 40% of replacement cost, even if the damage is covered. You're getting actual cash value, not replacement cost, unless your policy specifically guarantees otherwise.

Recoverable depreciation means you get the difference back after completing the replacement. Non-recoverable means that depreciated amount is gone forever. Most policies default to recoverable, but you need to file a claim, complete the work, and submit proof before you see that money. That creates a cash flow challenge for many homeowners.

Here's what they don't advertise: if your roof is past a certain age (usually 15-20 years depending on the carrier), some policies automatically switch to actual cash value only. You might think you have replacement cost coverage, but the fine print says otherwise once your roof hits that age threshold. Read your policy now, not when you're filing a claim.

I've walked homeowners through their policy documents and watched their faces change when they realize their 18-year-old roof qualifies for maybe four grand in actual cash value on a sixteen-thousand-dollar replacement. That's a brutal surprise during an emergency.

The Replacement vs Repair Decision From Your Insurer's Perspective

Insurers favor replacement when the damage is widespread and documented. If a hail storm damaged 40% of your roof's surface area, they know repairs won't solve the underlying vulnerability. They'd rather pay for one replacement than handle multiple repair claims over the next five years as other sections fail.

Isolated damage gets the repair treatment because insurers can argue (often correctly) that the rest of the roof is fine. A fallen tree branch that damaged 100 square feet doesn't justify replacing 3,000 square feet of roof. You'll get paid for the damaged section, and that's it.

Documentation drives outcomes. Take photos of all damage, not just the worst spots. If you're claiming wind or hail damage, document similar damage on neighbors' homes to establish that it was a widespread event. Get multiple estimates, because if your preferred contractor's bid is 40% higher than the adjuster's estimate, you'll be fighting for coverage rather than choosing between repair and replacement.

I've helped homeowners navigate claims where the adjuster initially approved repair, but after we documented the full extent of damage across all roof planes and provided detailed photos showing systemic impact, the claim was upgraded to full replacement. The difference was documentation quality, not damage severity.

The Timeline Factor Most Homeowners Ignore

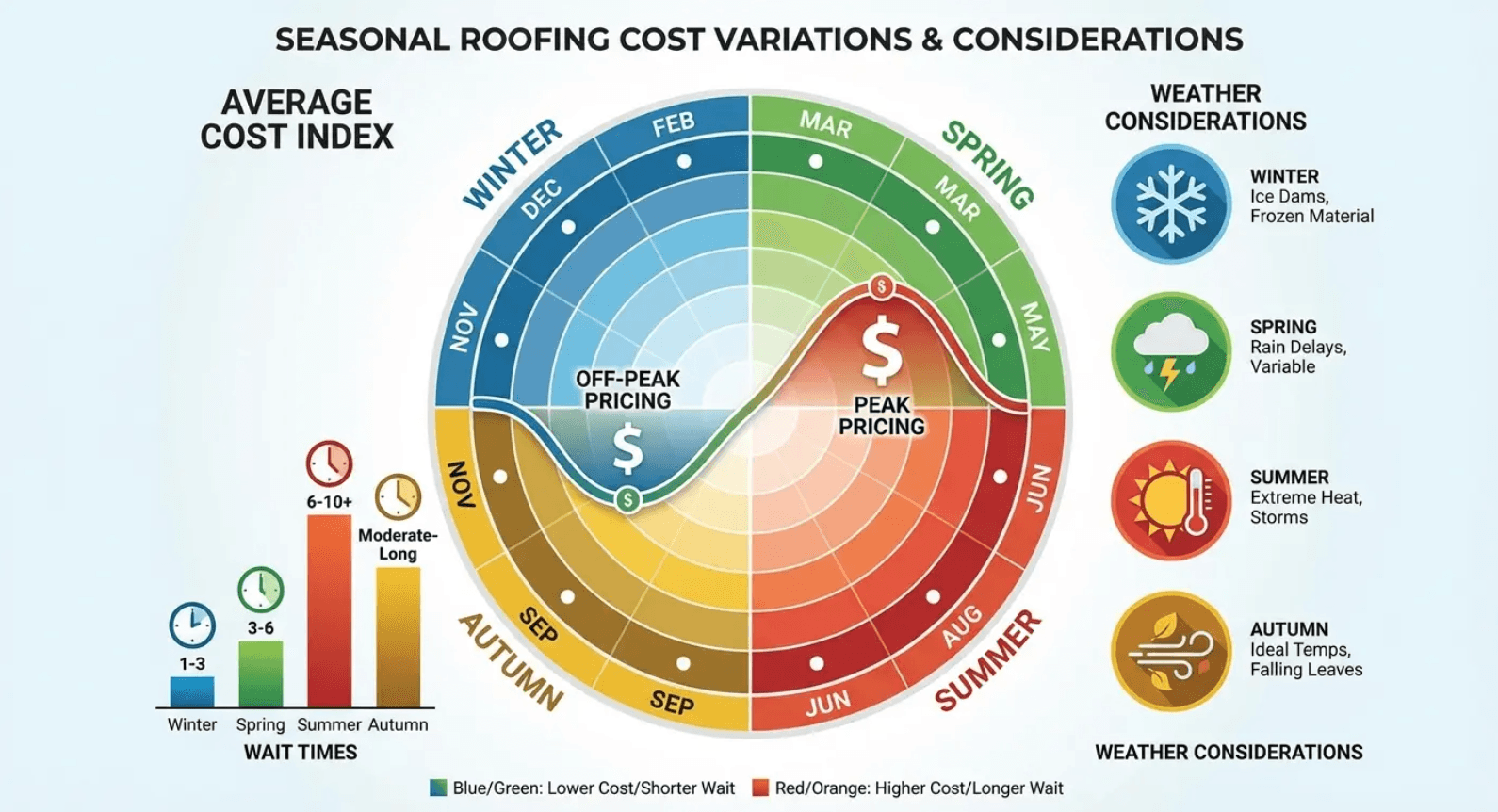

Timing affects the repair vs replacement decision in ways that have nothing to do with the roof's condition. Seasonal pricing fluctuations, contractor availability, and your personal timeline all factor into what makes financial sense.

Seasonal Pricing and Availability Realities

Roofing contractors charge more in May and October because everyone wants work done in perfect weather. You're competing with dozens of other homeowners, and contractors can afford to be selective about which jobs they take. Wait times stretch to 6-8 weeks, and pricing reflects the demand spike.

Winter installations in most climates are perfectly viable. Modern materials and installation techniques work fine in cold weather (above certain temperature thresholds that vary by product). You'll often see 15-20% lower pricing in January and February because contractors need to keep crews working. Summer can offer similar savings in extremely hot climates where most homeowners avoid the heat.

The weather concern that actually matters? Rain during installation. An open roof deck exposed to precipitation creates real problems. That's why you want to verify your contractor's weatherproofing protocols and their ability to complete tear-off and dry-in within a single day. Season matters less than the specific weather forecast for your installation week.

I've completed dozens of winter installations without issues. The homeowners saved thousands compared to spring pricing, and the work quality was identical. The crews were grateful for the work, we had more scheduling flexibility, and everyone won.

Your Personal Timeline Changes Everything

Planning to sell within 18 months? That compresses your decision timeline significantly. A new roof might return 60-70% of its cost in increased sale price or negotiating power, but only if buyers perceive it as new. A roof that's one year old at listing time reads as new. A roof that's four years old? You've used up the "new roof" selling point without getting the benefit.

Refinancing creates different pressure. Appraisers note roof condition, and a visibly aging or damaged roof can suppress your home's appraised value enough to affect your loan-to-value ratio. I've seen homeowners miss their target refinance rate because their roof knocked fifteen grand off their appraisal. A twelve-thousand-dollar replacement would have saved them more than that in interest over the loan term.

Major renovations deserve consideration too. If you're planning a second-story addition or significant structural work in the next 2-3 years, that might argue for delaying roof replacement (assuming your current roof can hold out) or accelerating it so you're not replacing a roof you'll need to modify soon anyway. Coordinate with your general contractor before making roofing decisions in isolation.

Retirement plans matter. If you're planning to age in place for the next 20+ years, replacement makes more sense even if repair could buy you 3-5 years. You want to handle major home systems while you're younger and more able to manage the project stress. Dealing with a roofing emergency at 75 is harder than planning a replacement at 65.

Why "One More Year" Usually Costs You Double

You're trying to get one more year from a roof that's clearly failing. You patch a leak in March, another in August, and you're watching the forecast nervously every time storms roll through. That "extra year" rarely saves money.

Emergency repairs cost more. Period.

And I'm not talking 10-15% more. You're paying premium rates because you need someone immediately, and you're not in a position to negotiate or shop around. Interior damage from leaks adds up fast. Drywall replacement, paint, potentially flooring if water makes it that far. A ceiling leak that could have been prevented with timely replacement can easily cost three to five grand in interior repairs alone.

Emergency replacement costs even more. You're calling contractors during a crisis, accepting whoever can start immediately rather than vetting multiple companies, and you're probably doing it during peak season when everyone else's roof is also failing. The twelve-thousand-dollar replacement you could have planned for turns into an eighteen-thousand-dollar emergency project, plus the interior damage costs, plus the stress of dealing with water entering your home.

I've watched this scenario play out dozens of times. Homeowners who delayed a needed replacement to "get one more year" ended up spending 40-60% more than they would have by addressing it proactively. The math never works in favor of delay once your roof is showing clear signs of systemic failure.

How We Help You Make the Right Call Without the Sales Pressure

You probably don't trust me. I'm a roofer writing about why you might need a new roof. I get it.

Here's what we do differently at Joyland Roofing: Our assessments start with understanding your timeline, your budget, and your plans for the home. We're not interested in selling you a replacement you don't need, and we're not going to patch a roof that's past saving just because it's the cheaper option today.

We'll inspect your entire roof system, not just the visible problem area. We check attic ventilation, decking condition, flashing integrity, and overall material condition across all roof planes. You get a written report with photos and our honest recommendation based on what we found, not based on what generates the highest invoice.

I've turned down jobs. I've literally told homeowners "your roof has another 5-7 years, don't let anyone sell you a replacement right now." Because the goal isn't maximizing this year's revenue. It's being the company you call back in 5 years when you actually need work done, and you remember we shot straight with you.

That includes helping you understand your insurance coverage, identifying whether you're dealing with isolated or systemic issues, and giving you realistic timelines for how long a repair will buy you. I've also had difficult conversations with homeowners who wanted to repair their way through problems that required replacement.

If you're staring at a roofing decision and you're not sure who to trust, we'd be happy to provide an honest assessment. No pressure, no sales games, just clear information about what your roof needs and why. Or don't call us. Call three contractors and use this framework to evaluate what they're telling you. Either way, don't make this decision blind.

Final Thoughts

If you take nothing else from this, remember these three things:

1. Add up what you've spent on repairs in three years. If it's over 30% of replacement cost, stop repairing.

2. Your roof's age matters more than the current damage. A 20-year-old roof with minor damage is still a 20-year-old roof.

3. Emergency replacements cost 40-60% more than planned ones. Don't wait for crisis.

Everything else (insurance details, seasonal pricing, partial replacement options) matters, but those three things drive 90% of the decision.

The roof repair vs replacement question isn't about your roof. It's about what you need from your home over the next decade and how much flexibility you want to maintain. Every dollar you spend today either buys you options or locks you into a corner.

I've seen too many homeowners make decisions based on incomplete information or short-term thinking, then face consequences they didn't anticipate. The goal here isn't to push you toward replacement or convince you that repairs are always wrong. It's to give you a framework for evaluating your specific situation with clear eyes.

Your roof's condition, its age relative to expected lifespan, your timeline for the home, your insurance coverage, and your budget all factor into the equation. Weight them honestly. Don't believe a repair will do more than it can, but don't replace a roof that's got legitimate life left just because a contractor tells you it's time.

Make the decision that serves your long-term interests, not just the one that feels easier right now. Your future self will thank you for thinking strategically instead of reactively.